Starting from September 1, 2024, South Africa will introduce a new retirement savings system, known as the two-pot system. This change will affect all current and future members of retirement funds, making it essential to understand how the new structure works. Here is a simplified overview of the purpose and mechanics behind this new system to help clear up any confusion.

Understanding the Two-Pot Retirement Savings System

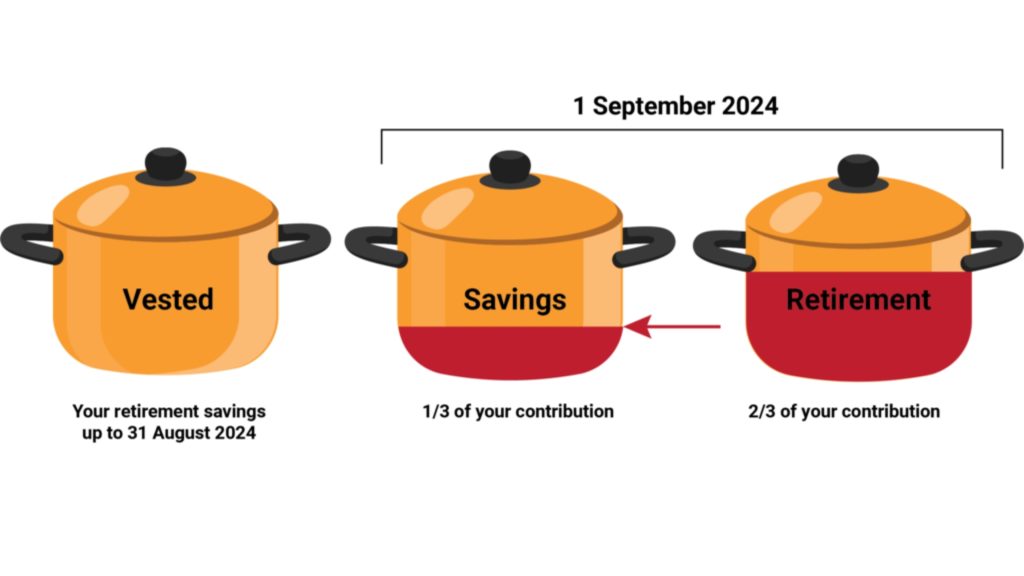

The new two-pot retirement savings system is designed to strike a balance between preserving retirement investments until retirement and allowing limited access to a portion of these savings during one’s working years. Beginning September 1, 2024, contributions to all types of retirement funds, including provident, pension, and retirement annuity funds, will be divided into two parts:

- Savings Component (One-Third): This part allows members to access funds before retirement in case of emergencies.

- Retirement Component (Two-Thirds): This part remains inaccessible until retirement and must be used to purchase a pension product.

Transitioning to the New System

A significant challenge in implementing the two-pot system lies in managing the transition from the current retirement fund rules to the new structure while ensuring that the system remains fair to all members.

Vested Rights and Exclusions

The term “vested rights” refers to the rights members currently have regarding their retirement investments, which are safeguarded under the new law. All investments made before the introduction of the two-pot system will be part of a vested component, and the existing rules on accessibility and tax will still apply to this component.

Certain members will be excluded from the two-pot system. For instance, members of a provident fund who were 55 or older as of March 1, 2021, will not be affected by the new rules unless they choose to opt in. If they opt in, new contributions will follow the two-pot allocation while their existing benefits remain vested under the old rules.

Accessing Savings Under the New System

When the two-pot system is implemented, retirement fund members will have limited access to a portion of their existing savings, known as “seed capital.”

Key Points About the Seed Capital Withdrawal

- Value Limit: The seed capital is capped at 10% of the retirement fund balance as of August 31, 2024, with a maximum amount of R30,000. For example:

- If you have R30,000 in your account, R3,000 will be accessible.

- If you have R150,000 in your account, R15,000 will be accessible.

- If you have R900,000 in your account, R30,000 will be accessible.

- Tax Implications: Any amount withdrawn will be taxed at your marginal income tax rate. The retirement fund or its administrator will apply for a tax directive from the South African Revenue Service (SARS) and deduct the tax before you receive the funds.

- Timing of Withdrawals: Withdrawals may only be possible once the retirement fund’s rules are approved by the Financial Sector Conduct Authority (FSCA) and if the fund’s systems are ready to manage the seed capital distribution. Delays might occur if these approvals or system updates are not in place by September 1, 2024.

Potential Benefits and Challenges of the Two-Pot System

The two-pot system aims to provide a balanced approach by allowing limited access to savings while promoting greater preservation of retirement funds. This system may offer financial flexibility in times of need without requiring resignation from employment.

However, it’s essential to remember that the primary goal of your retirement savings is to provide income during retirement. Regular withdrawals from the savings component can reduce the amount available for retirement, and these withdrawals will be taxed, potentially pushing you into a higher tax bracket depending on your total income and the withdrawal amount.

Understanding the variations of the two-pot system, including the role of the FSCA in approving fund rules and the need for SARS to issue tax directives, is crucial for members to make informed decisions.